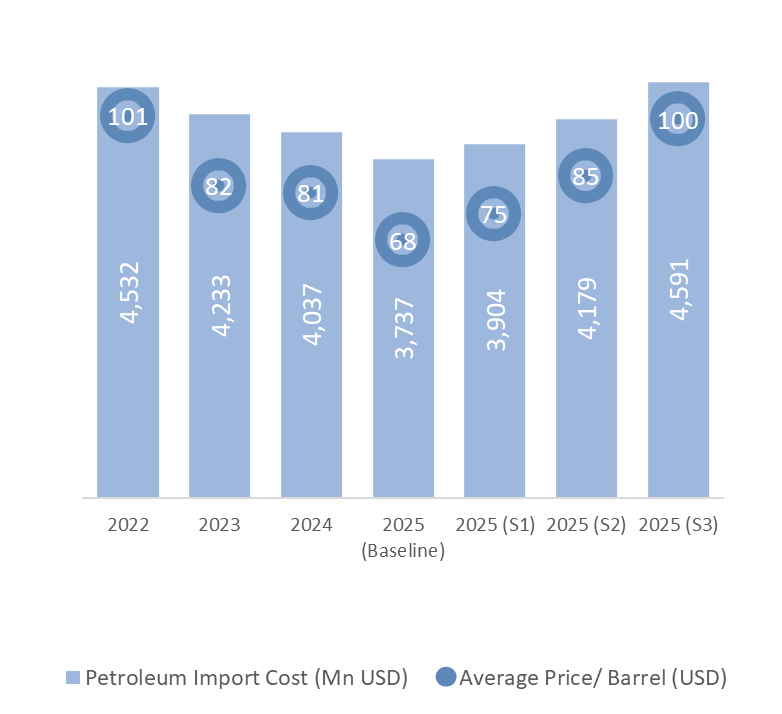

1. Oil & fuel prices – inflation and growth

The conflict is already threatening the Strait of Hormuz, a chokepoint that carries ~20% of global daily oil consumption. If traffic/insurance is disrupted, crude and refined product prices can jump even without a physical supply cut.

With FX steady at LKR 313/USD, our forecast shows that if crude rises from USD 80 to USD 100 (Platts from 85 to 105) amid the Iran conflict, Sri Lanka pump prices could increase by ~LKR 40/L: Petrol 92 from LKR 314 to 355 and diesel from LKR 303 to 343 (both ~+13%).

Chart 1912358337, Chart element

2. Shipping & insurance – import costs and shortages risk

Even if Sri Lanka can still buy fuel, insurance withdrawal, tanker delays, rerouting, and higher freight can raise landed costs and create intermittent supply tightness. Reuters reporting suggests shipping through Hormuz has become materially riskier, with threats to vessels.

If regional attacks spread to energy infrastructure/LNG, that can spill into global energy pricing more broadly (oil and gas), which tightens external balances for importers like Sri Lanka.

3. FX & reserves – rupee pressure and rates staying higher for longer

A higher oil bill usually means more USD demand. If inflows do not offset, the rupee can face depreciation pressure and reserves can be drawn down to smooth volatility.

Imported inflation (via fuel) can reduce the Central Bank’s room to ease policy; even if policy rates do not rise, the path of cuts can get delayed, keeping financing costs elevated.

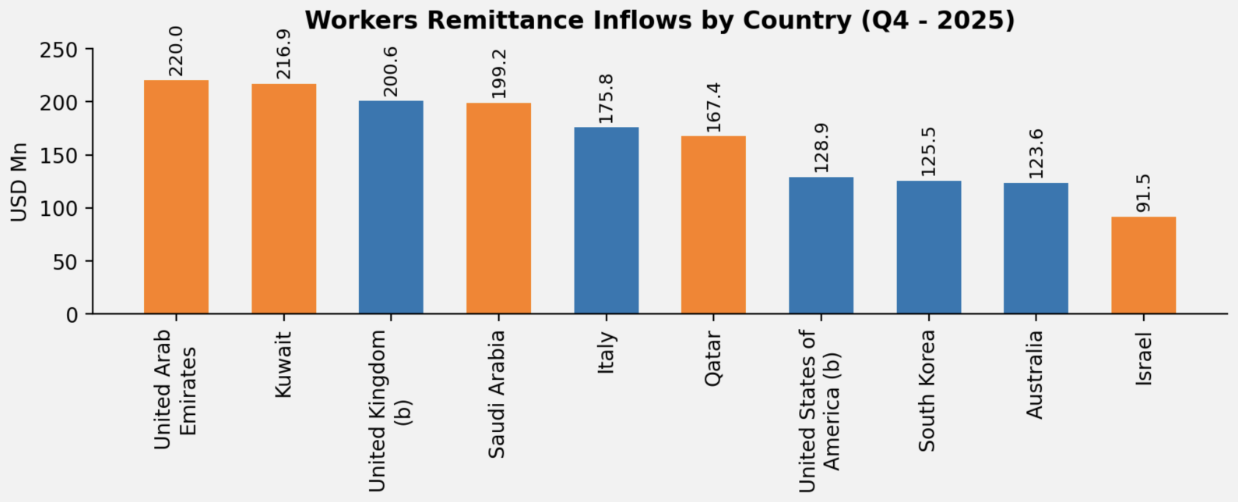

4. Remittances from the Gulf – downside risk if conflict spreads/jobs weaken

Sri Lanka’s remittances are heavily tied (45.1%) to the Middle East; countries such as UAE, Kuwait, Saudi Arabia among the largest sources.

If the conflict triggers layoffs, mobility restrictions, or a Gulf growth slowdown, remittance momentum can soften a key risk because remittances are a major FX stabilizer.

5. Effect on exports and Tourism

The Middle East is an important region for Sri Lankan exports (tea is a notable one which accounts for ~55% by volume), so demand disruption or payment/shipments friction can hurt certain exporters.

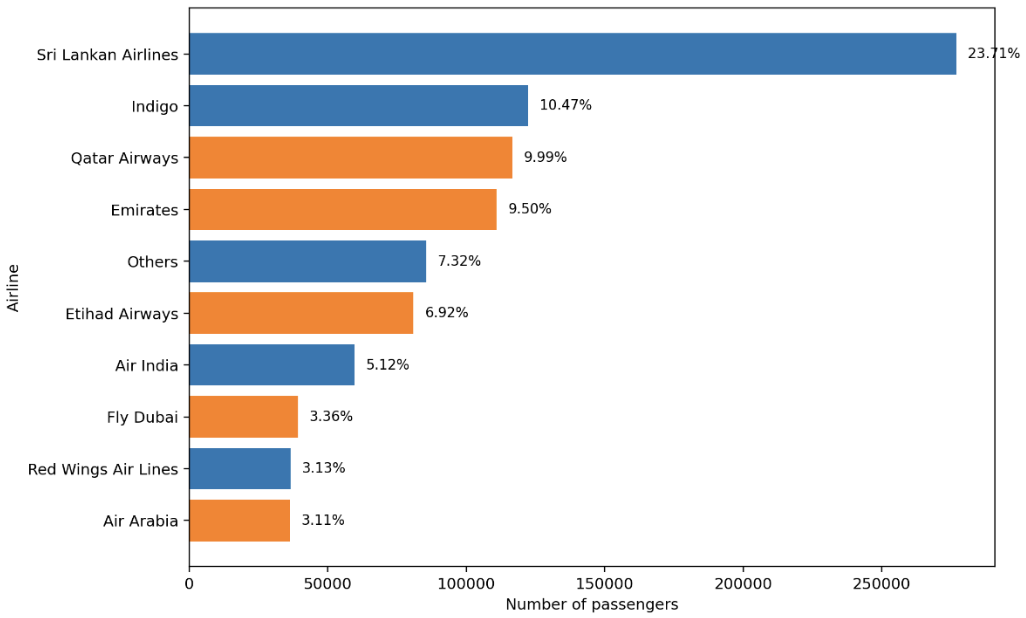

Tourism impact depends on how far the conflict spreads and whether flight routes/airfares get disrupted. For example, in 2025 contribution of major middle eastern hub carriers account for approximately 26.41% of total tourist arrivals (Qatar Airways (116,638 passengers, 9.99%), Emirates (110,961 passengers, 9.50%), and Etihad Airways (80,844 passengers, 6.92%)). Hence any flight disruptions/capacity cuts could quickly hit arrivals.

Summary

- Oil & fuel – inflation/growth: Strait of Hormuz handles ~20% of global oil flows; disruption risk can spike oil/fuel prices even without supply cuts.

- Shipping & insurance – higher import costs: War-risk insurance, delays and rerouting can lift landed fuel costs and create short-term shortages.

- FX & reserves – rupee pressure, cuts delayed: A higher oil bill raises USD demand, pressuring LKR/reserves and reducing room for faster rate cuts.

- Gulf remittances – downside risk: ~45.1% of remittances come from the Middle East; weaker Gulf jobs/growth could slow inflows (a key FX buffer).

- Exports & tourism – demand/route risks: Middle East is important for exports (tea ~55% by volume); payment/shipment disruptions can hurt exporters. Tourism risk rises if flight routes/airfares are disrupted, plus broader risk-off sentiment.

Find Us on Maps

Find Us on Maps